If you think that components of your home are not up to present building codes, consider getting an endorsement to your policy called an Ordinance or Law, which pays a defined amount towards bringing a home up to code throughout a covered repair. Charming, unique functions on older homeslike wall and ceiling moldings and carvingsare costly to recreate and some insurer might not offer replacement policies for that reason.

This means that rather of fixing or replacing features normal of older homeslike plaster wallswith like materials, the policy will spend for repair work utilizing today's basic structure products and building and construction methods. Inflation can affect restoring costs. If you prepare on owning your home for a while, consider adding an inflation guard clause to your policy.

After a significant catastrophe such as a hurricane or twister, building and construction costs may increase suddenly because the price of structure products and construction workers increase due to the widespread demand. This price bump may push rebuilding costs above your homeowners policy limitations and leave you brief. To safeguard against this possibility, an ensured replacement expense policy will pay whatever it costs to rebuild your house as it was prior to the disaster.

Many property owners insurance coverage offer protection for your belongings at about 50 to 70 percent of the insurance coverage on your residence. Nevertheless, that basic quantity may or might not suffice. To discover if you have enough coverage: In order to properly assess the value of what you own, it's extremely advisable to conduct a house stock.

In case any or all of your stuff is taken or damaged by a catastrophe an inventory will make filing Go here a claim much simpler. There are several apps readily available to help you take a home stock, and our post on how to create a house stock can assist, also.

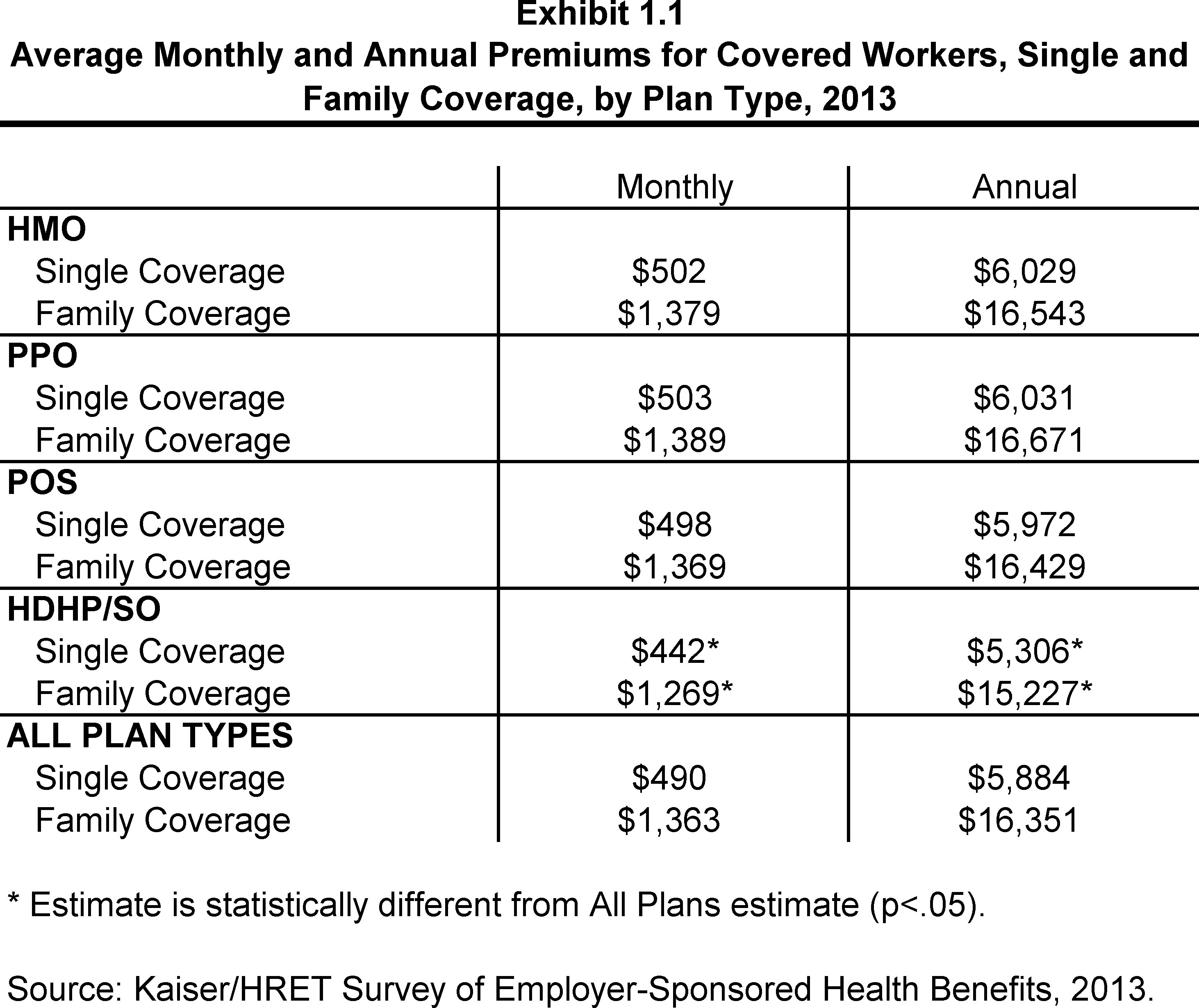

What Happens If I Don't Have Health Insurance Can Be Fun For Everyone

The price of replacement expense coverage for homeowners has to do with 10 percent more but is normally a beneficial financial investment in the long run. (Keep in mind that flood insurance for belongings is only readily available on a real cash worth basis.) If you believe you require more protection, call your insurance coverage professional and inquire about greater limitations for your individual belongings.

For example, fashion jewelry protection may be restricted to under $2,000. Some insurer may also put a limitation on what they will pay for computers. Check your policy (or ask your insurance coverage expert) for the limits of your coverage for any expensive items. If your house inventory includes products for which the limits are too low, consider buying a special personal effects floater or an endorsement.

Additional Living Expenses (ALE) is a really important function of a standard homeowners insurance plan. If you can't live in your house due to a fire, severe storm or other insured disaster, ALE pays the extra costs of momentarily living somewhere else. It covers hotel expenses, restaurant meals and other living costs sustained while your home is being reconstructed.

Numerous policies provide coverage for about 20 percent of the insurance coverage on your home. However ALE coverage limitations differ from business to company. For example, there are policies that provide an unlimited quantity of protection, for a limited quantity of time, while others may just set limits on the quantity of coverage.

The liability portion of property owners insurance coverage covers you against lawsuits for physical injury or home damage that you or member of the family or pets trigger to other individuals, in addition to court expenses sustained and damages awarded. You ought to have sufficient liability insurance coverage to safeguard your assets. Many homeowners insurance plan supply a minimum of $100,000 worth of liability insurance, however greater amounts are offered and, significantly, it is recommended that homeowners consider acquiring at least $300,000 to $500,000 worth of liability coverage.

How To Get Insurance To Pay For Water Damage Fundamentals Explained

Umbrella or excess liability policies provide protection over and above your standard house (or auto) liability policy limits. These policies start to pay after you have consumed the liability insurance coverage in your underlying policy. In addition to offering extra dollar amount protection, umbrella or excess liability typically provides broader coverage than standard policies.

The higher the underlying liability protection you have, the more affordable the umbrella or excess policy. To write an umbrella or excess policy, the majority of companies will require a minimum of $300,000 underlying liability insurance on your standard homeowners policy.

If you own a house, you might question just how much homeowners insurance you truly need. After all, the more protection you have, the greater the premiumsand you probably want to prevent paying more than you need to. Still, if you don't have sufficient coverage, could you manage to rebuild your house and change your personal belongings if a catastrophe were to strike? Fortunately is that you can fine-tune your house owners insurance plan to make certain you have the ideal typeand right amountof coverage.

Basic policies do not cover whatever, so you might require additional protection to protect against hazards such as floods and other natural catastrophes. Your insurance coverage agent can help you decide the type and quantity of protection you need. A home is most likely the largest single purchase you'll ever make, so it makes sense that you would wish to protect that investment.

Another method is to purchase a great homeowners insurance plan. Homeowners insurance is a type of home insurance coverage that safeguards your home and other important items. A standard policy covers damage and losses to your house and individual valuables. It also secures your assets from liability claims, such as accidents and pet-related events.

The Ultimate Guide To What Is A Health Insurance Premium

According to the Insurance Coverage Info Institute, a few of the most common perils covered by standard homeowners policies include: Damage from an airplane, car, or vehicleExplosionsFalling objectsFire and smokeLightning strikesRiots or civil commotionTheftVandalism and malicious mischiefVolcanic eruptionsWater damage (from within the home only) Weight of ice, snow, and sleetWindstorms and hail The portion of property owners who improperly think flood damage is covered by their standard policy, according to Princeton Study Research Associates International Source: How Insurance Coverage Misconceptions Can Cost You While standard policies cover lots Additional info of various dangers, they do not cover whatever, including: Flood insurance coverage is particularly left out from standard policies, so you must purchase it as a different policy.

involve some type of flooding. how much does flood insurance cost. Earthquake coverage is usually offered as a separate policy or as an recommendation to your existing house owner's protection. Homeowner's insurance does not cover mold, infestation from termites and other insects, or damage due to Click for more lack of upkeep. Drain backups aren't covered by standard policies or by flood insurance coverage.

According to Insurance coverage. com, if you have a mortgage, your loan provider will require a minimum amount of home and liability coverage. That coverage protects your investmentas well as your loan provider's. About 60% of all houses in the U.S. are underinsuredby approximately 20% according to a report from housing information firm CoreLogic.